EIA: Natural gas pipeline projects lead to smaller price discounts in Appalachian region

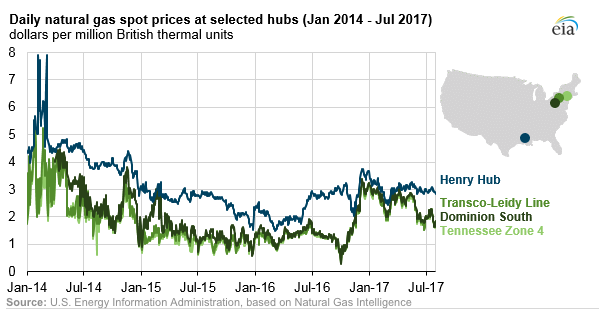

As new pipeline projects and expansions are completed, the difference between the Henry Hub national benchmark price and daily spot natural gas prices at pricing hubs in the Appalachian region has narrowed.

Through the first seven months of 2017, the difference between prices at the Henry Hub in Louisiana and at Dominion South in southwestern Pennsylvania averaged $0.53 per million British thermal units (MMBtu), about two-thirds the average difference of $0.76/MMBtu during the first seven months of 2016. The differences between the Henry Hub and other Appalachian region price points followed similar trends.

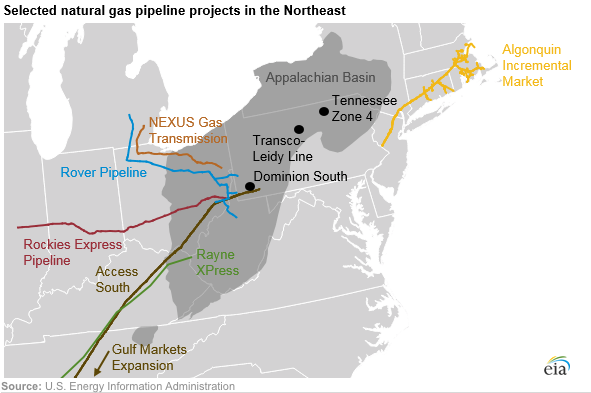

Appalachian regional prices are influenced by regional production rates and the availability of infrastructure to transport natural gas to demand centers.

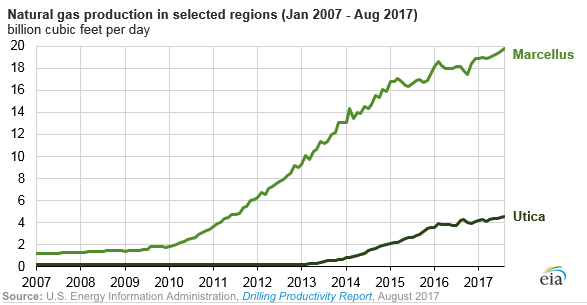

Production in Ohio, Pennsylvania, and West Virginia from the Marcellus and Utica shale plays has grown rapidly over the past several years, and infrastructure to deliver natural gas to consumers has not kept pace.

During 2016, 11 interstate pipeline projects in the Northeast were completed, adding just over 4.0 Bcf/d of interregional capacity. Much of this capacity came on between July and December, as only 0.9 Bcf/d of capacity was completed in the first half of the year.

During 2016, 11 interstate pipeline projects in the Northeast were completed, adding just over 4.0 Bcf/d of interregional capacity. Much of this capacity came on between July and December, as only 0.9 Bcf/d of capacity was completed in the first half of the year.

With limited infrastructure to deliver the available supply to consumers and high regional natural gas inventories, the difference between prices at Dominion South and Henry Hub widened from an average of $0.62/MMBtu in the first half of 2016 to $2.55/MMBtu at the end of September.

Starting in October 2016, more pipeline projects were completed, including two of the biggest projects in the region, the Equitrans expansion of the Ohio Valley Connector and the Rockies Express Pipeline Zone 3 Capacity Enhancement. This growth in pipeline capacity likely contributed to a narrowing of the spread between the Henry Hub and Dominion South price points, which reached $0.49/MMBtu at the end of the year.

As the Algonquin Incremental Market expansion and Rockies Express Pipeline Zone 3 Capacity Enhancement reached full capacity, the price difference to Henry Hub dropped further and averaged $0.33/MMBtu over the first four and one-half months of 2017.

As the Algonquin Incremental Market expansion and Rockies Express Pipeline Zone 3 Capacity Enhancement reached full capacity, the price difference to Henry Hub dropped further and averaged $0.33/MMBtu over the first four and one-half months of 2017.

However, as regional production has continued increasing, the difference between Dominion South and Henry Hub has since widened.

Though Eastern Shore Natural Gas’s White Oak Mainline Expansion Project was completed in March, natural gas production in the Marcellus and Utica plays has already increased 0.9 Bcf/d since January to reach 24.1 Bcf/d in July. However, 25 pipeline projects currently under development are scheduled to be completed in 2017, resulting in up to 7.2 Bcf/d of additional takeaway capacity in the Northeast.

Source: U.S. Energy Information Administration (link)